8 min read

Why BC Home Insurance Won't Cover Poly-B Pipes

For years, Poly-B was just old pipe. Now it is an insurance problem. More and more BC homeowners are opening renewal letters that mention polybutylene, asking for proof of replacement, or quietly excluding the exact kind of damage Poly-B is most likely to cause. Some are finding out the hard way, after a leak, that their claim is denied.

If that is where you are, or you want to get ahead of it, here is what is actually happening with insurers and Poly-B in BC, and the practical steps to protect your coverage.

Why Insurers Treat Poly-B as a Risk

Insurance is a bet on risk, and Poly-B has a track record that makes insurers nervous.

The pipe degrades from the inside out when exposed to chlorinated municipal water. The damage gives no warning on the outside, and when Poly-B fails it tends to fail suddenly: a pinhole leak behind drywall, a cracked fitting, or a full rupture that empties your home's water supply into the walls and floors. Insurers have paid out on enough of these claims to now classify Poly-B as an elevated-risk material across Canada, BC included.

From the insurer's point of view, a Poly-B home is more likely to produce a large water damage claim than a comparable home with modern pipe. So they price for it, restrict it, or avoid it. If you want the full background on when this pipe was installed and why it was phased out, we covered that here: When Was Poly-B Used in BC?

The Different Ways Insurers Say No

"Won't cover" is a simplification. In practice, BC insurers respond to Poly-B in a range of ways, and some of them are easy to miss until it is too late.

Higher premiums. The policy stays in place, but you pay more for the added risk.

Higher deductibles or reduced payout caps on water damage. Coverage exists on paper, but a real claim leaves much more of the bill on you.

A water damage exclusion rider. This is the dangerous one. The policy renews and looks intact, but it specifically excludes damage caused by the plumbing system. The most likely claim category for your home is the one that is no longer covered, and many homeowners do not register what the rider means until a claim is denied.

Conditional renewal with a deadline. The insurer renews but requires Poly-B to be replaced and documented by a set date, or coverage ends.

Non-renewal or cancellation. The insurer declines to continue the policy at the end of the term, leaving you to find a new one on a home with confirmed Poly-B, which is harder and more expensive.

Outright refusal to cover. Some providers will not write a new policy on a Poly-B home until the pipe is fully replaced.

The common thread is that the trend is moving one direction. Insurers are getting stricter on Poly-B over time, not more lenient.

The Claim Denial Trap

Even when a policy seems to cover water damage, Poly-B claims get denied for reasons worth understanding before you are in the middle of one.

The most common is the wear-and-tear argument. Insurance generally covers sudden and accidental damage, not gradual deterioration. Because Poly-B degrades slowly over years, an insurer can classify a failure as expected wear rather than a sudden event, and deny the claim on that basis.

Disclosure is the other big one. If your home has Poly-B and you did not disclose it when you bought the policy, an insurer can deny a claim, or even void coverage, on the grounds that the risk was not reported. Honesty up front protects you later.

None of this is meant as a substitute for reading your own policy or talking to your insurer or broker. Coverage terms vary between providers, and the only way to know exactly where you stand is to check your specific policy.

Why This Matters Even If You Are Not Selling

It is easy to put Poly-B off if you have no plans to move. Two things make that risky.

First, a single failure can cause water damage that costs more than the entire repipe, and if the claim is denied or limited, that cost falls on you.

Second, insurability follows the home. If you ever do sell, a buyer who cannot get affordable coverage may struggle to finalize a mortgage, since lenders require active insurance. A Poly-B home can stall a sale for reasons that have nothing to do with the rest of the property.

What to Do About It

Here is the practical path, in order.

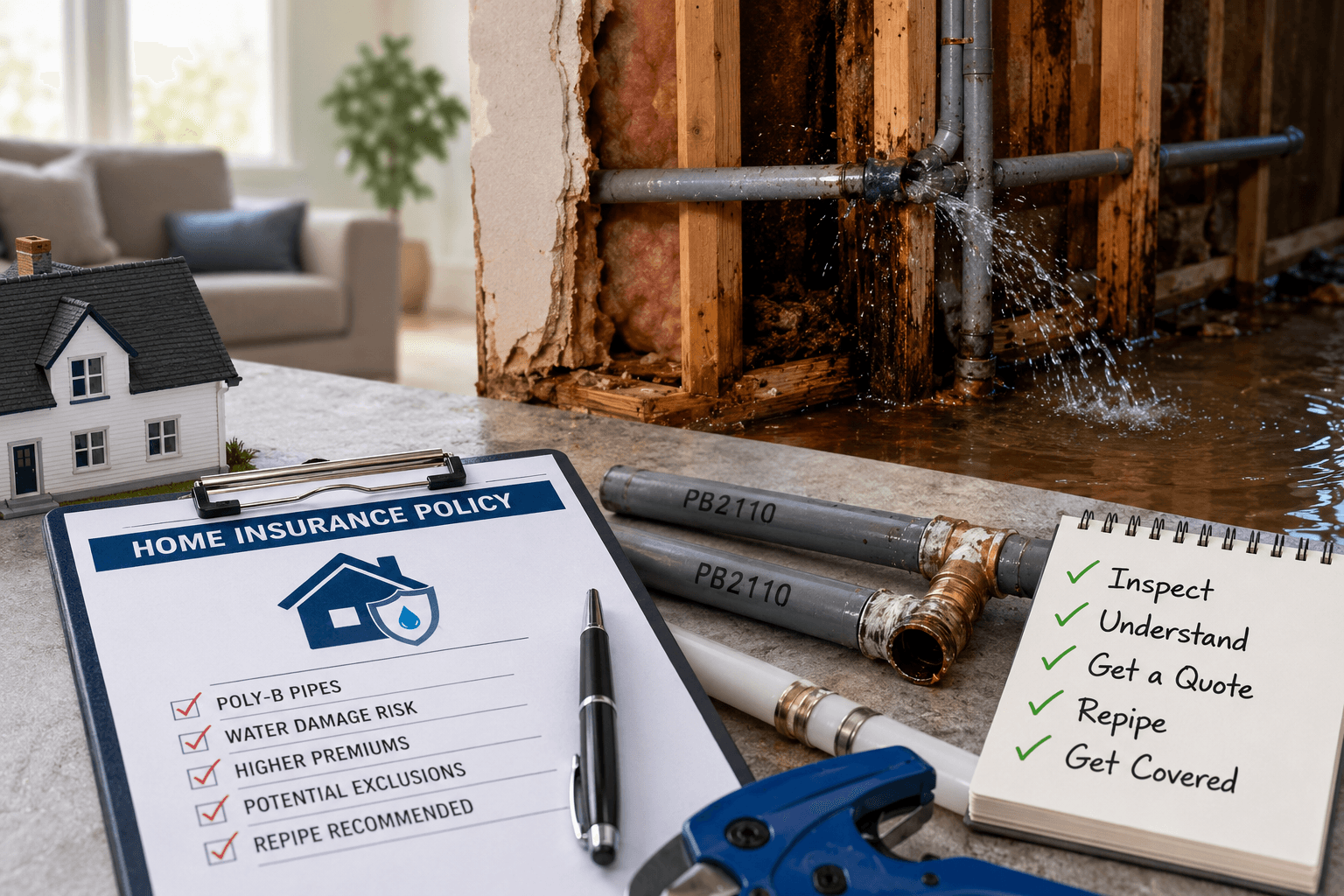

1. Confirm what you have. Look for grey or blue-grey flexible plastic pipe, often stamped "PB2110," under sinks, near the water heater, and around the main shutoff. Much of the pipe is hidden in walls, so if you find some, assume there is more. A licensed plumber can confirm the full extent.

2. Read your policy and talk to your insurer or broker. Find out whether Poly-B is excluded, surcharged, or subject to a deadline. Ask directly what would happen to a water damage claim today. It is better to know now than at claim time.

3. Get a written repipe quote. Replacing Poly-B with modern PEX is the step that moves your home from a liability back to standard insurability, and it usually lowers your risk profile with insurers. If you want to know what that costs in BC, we broke it down here: How Much Does a Poly-B Repipe Cost in BC?

4. Keep the documentation. After a repipe, you will receive proof of the work and the permit and inspection records. Insurers want this, both to restore or improve coverage and to confirm the Poly-B is genuinely gone. Keep it somewhere safe.

Replacing Poly-B is not just a maintenance upgrade. For a growing number of BC homeowners, it is the difference between being insurable and being on your own.

Get Ahead of It With Ark

Ark Plumbing & Heating replaces Poly-B with PEX for homeowners across the Lower Mainland, and we hand you the documentation your insurer will ask for. We will confirm whether you have Poly-B, show you where it is, and give you a written quote with the scope spelled out, so you can make a clear decision before a renewal deadline or a leak forces one.

Learn more about our Poly-B repipe service, or get in touch with us here to book an assessment.

We serve homeowners across the region, including:

This article is general information, not insurance advice. Coverage terms vary by provider, so check your own policy and speak with your insurer or broker about your specific situation.

Article details

Date

Author

Noah Debebe